Samsung remains the world’s most dominant brand when it comes to the ‘advanced TV’ market, which is a catch all term for televisions that feature newer display technologies.

That’s according to the analyst firm Display Supply Chain Consultants’s latest Quarterly Advanced TV Shipment and Forecast Report, which forecasts revenues from the market for Advanced TVs to grow 9% annually from 2019 to 2025 to $26 billion a year.

DSCC defines Advanced TV as “any TV with an advanced display technology feature, including all OLED TVs, 8K LCD TVs and all LCD TVs with quantum dot technology.”

The list of technologies includes TVs that use a Quantum Dot Enhancement Film, which includes those marketed as QLED by Samsung, TCL and other brands. Also included in the list is MiniLED technology, which covers LCD TVs with a MiniLED backlight; Dual Cell LCD; WOLED, or White OLED, as sold by LG; and LCD Others, which includes LCD TVs featuring an 8K resolution display that do not fall into the above categories.

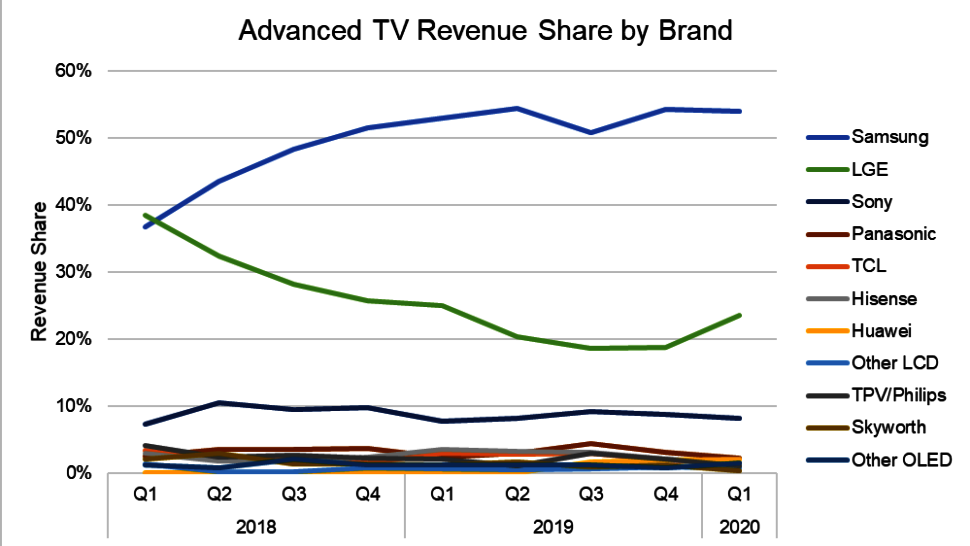

DSCC said Samsung managed to increase its revenue share of the advanced TV market from 53% to 54% in the first quarter of 2020, mainly by expanding its QDEF product line with more affordable models this year. LG came in second overall with a 24% revenue share of the market, while Sony was third with 8%.

The most interesting national market is China, and the battle for dominance there has gotten quite intense with no less than four brands all commanding a double-digit revenue market share. In China, Samsung commands a 42% market share in Advanced TVs, followed by Huawei in second place with 18%. Hisense commands 14%, and LG also ranks in the double digits. On the other hand, Skyworth, once a leading brand in China, has seen its share of the advanced TV market fall to just 3%.

DSCC said it’s expecting growth in the advanced TV market to slow down due to COVID-19, but the outlook is not nearly as bleak as the rest of the TV industry. Overall, it’s expecting growth of 11% in the second quarter of 2020, compared to the same period one year ago. However, things should pick up by the final quarter of the year, with 27% year-over-year growth expected in that period.

One driver of that growth is expected to be the availability of smaller, 48-inch OLED TVs, which are being shipped by LG Display to several brands for the first time this year. That, combined with LG Display’s increased production capacity, should help to boost OLED’s share of the advanced TV market, DSCC said. All in all, DSCC expects advanced TV unit shipments to rise by 30% in 2020, compared to the year before.

As for the long term forecast, DSCC said advanced TV shipments will grow from under 10 million in 2019 to 35 million by 2025, representing a 24% compound annual growth rate for that period. OLED TV shipments will grow at a 31% CAGR in that period to 14.7 million units, while advanced LCD TV shipments will grow at a 21% CAGR to 20.8 million units.

The biggest growth will be seen in larger display sizes, with shipments of advanced TVs in the 75-inch plus range expected to grow by 36% through 2025. 75-inch plus OLED TV shipments will grow even more, at an 87% CAGR, DSCC said.