Hisense and TCL are growing their global TV market share at the expense of LG Electronics and Samsung, though the latter company remains the industry’s biggest overall supplier.

The TV manufacturing industry is experiencing a downturn after seeing record sales during the COVID-19 pandemic a couple of years ago, and total shipments are expected to fall by over 2% this year.

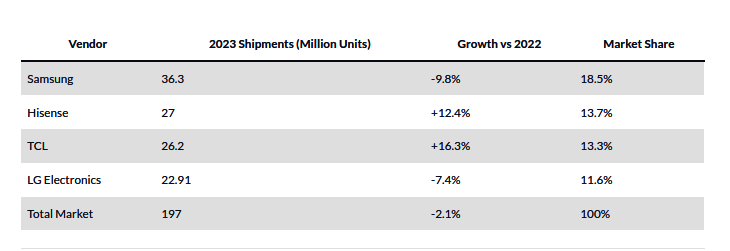

With the pandemic now firmly rooted in the past and consumers no longer confined to their homes, plus the economic uncertainty in many global markets, companies are selling fewer TVs than before. As a result, the latest report from TrendForce suggests that total worldwide TV shipments will fall to less than 197 million units in 2023.

TrendForce identified the industry’s top TV brands as Samsung, which still holds a commanding lead over its rivals, followed by Hisense, TCL and LG in fourth place, down from second spot just a couple of years ago.

Sasmung is likely to see TV sales fall by as much as 10% this year, with declines in its 8K, Mini-LED and QLED LCD categories. However, sales of its QD-OLED TVs are expected to grow rapidly this year, reaching around 890,000 units, up 153% from last year, when they made their debut. All told, Samsung is expected to command a 18.5% market share, with 36.3 million shipments in total

LG’s OLED TVs are much more established, and the company is likely to see sales decline as a result of its strong position in that segment. That’s because economic woes are dissuading consumers from making large investments in what many might see as luxury products. TrendForce says LG’s shipments will fall by 7.4% to just 22.9 million units, giving it an 11.6% share of the overall market.

On the other hand, the big Chinese brands Hisense and TCL continue to grow thanks to their ability to offer advanced OLED and LCD TVs with premium features at lower price points than their Korean rivals. Hisense is expected to ship 27 million units this year, up 12.4% from a year earlier, giving it a 13.7% market share. As for TCL, it’s forecast to ship 26.2 million units in 2023, up 16.3% from the prior year, attaining a 13.3% market share.

According to TrendForce, one reason for the overall decline is that TV panel prices have been rising all year, causing brands to scale back on promotions, leading to fewer sales of higher-end TV models.

The outlook for 2024 remains unclear. TrendForce is tentatively predicting a slight rise in overall shipments of just 0.2%, with a number of major sporting events next year likely to cause a bump in sales. However, it said economic risks and production constraints may yet result in shipments declining instead.