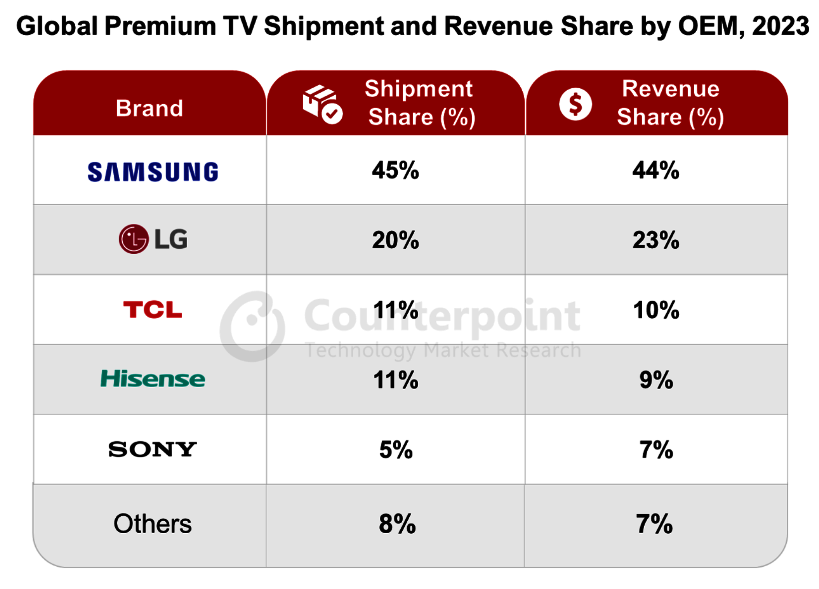

Samsung Electronics has ranked as top dog by a comfortable margin in yet another TV industry sales tracker, achieving a 45% share of all “premium TV” shipments over the last year, according to Counterpoint Research. The company also dominated in terms of revenue, commanding a 44% share of the market.

That’s according to Counterpoint’s Global TV Shipment Tracker, which is a new quarterly report split by region, screen size, resolution, average selling price (ASP) and other parameters. The report was produced in collaboration with the TV industry analyst firm DSCC, which was recently acquired by Counterpoint, and it also reveals that global premium TV shipments declined 3% last year to reach 223 million units worldwide.

Trailing Samsung in second place is LG Electronics, which accounted for 20% of all premium TV shipments globally and 23% of revenues.

Counterpoint defines premium TVs as those that feature “advanced display technologies” such as QD-OLED, WRGB OLED, MicroLED, Mini-LED and quantum dot LCD displays, with a price tag of $2,500 or more.

“We are excited to roll out Counterpoint Research’s Global TV Shipment Tracker, a powerful tool to assess the market and technology trends as well as the competitive environment,” said Tom Kang, Director, Counterpoint Research. “As the first joint product of Counterpoint and DSCC, the tracker also shows how we are bringing additional value to clients, with the net result much greater than the sum of its parts.”

The new ranking shows TCL in third price with 11% of shipments and 10% of all revenues, while Hisense ranks fourth with 11% and 9%, respectively. Sony, which sells its premium TVs at higher average prices than its rivals, came in fifth, accounting for 5% of all shipments and 7% of revenues.

All told, premium TV shipments actually rose by 1% in 2023 from the year before, increasing their market share to 10% of the overall TV market. Counterpoint said this was due to a surge in sales of premium TVs in China, where shipments and revenues grew by 39% and 49% respectively. This was driven by a clear shift towards Mini-LCD displays by China’s biggest TV brands, coupled with aggressive pricing and promotions.

Looking forward, Counterpoint said it expects the global premium TV segment to grow by the mid-single digits this year thanks to a recovery in demand in Europe and the U.S. “We are expecting premium to do better this year on increasing screen sizes and ASPs,” said Calvin Lee, DSCC Senior Director, South Korea. “Recovery in the US and Europe will be a big factor but, as we are seeing in China, the right balance of features and pricing can be a big driver of replacement rates.”