Market researcher DSCC has said the market for premium TVs will rebound this year, kicking off a long-term growth trend that’s expected to continue through 2027 at least.

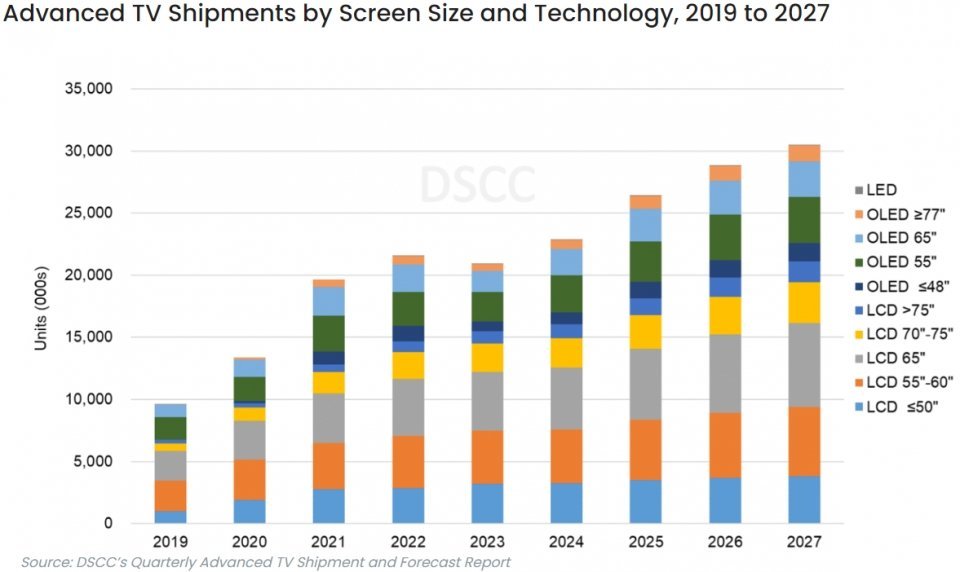

DSCC’s report shows that premium TV shipments decreased by around 4% in 2023 compared to the previous year. However, that number is expected to grow at a compound annual growth rate of 10%, reaching 30 million units by 2027.

A report in The Elec explains that DSCC defines premium TVs as those equipped with White OLED, QD-OLED and Mini-LED panels, as well as QLED TVs with quantum dot films, 8K LCD TVs and MicroLED TVs.

In 2023, shipments of OLED TVs fell by an alarming 20%, primarily due to the weak global economy and higher interest rates that affected sales. However, the OLED segment is likely to rebound immediately this year, growing at a CAGR of 14% between 2023 and 2027 to reach 9.2 million units.

Of the 30 million premium TV shipments forecast for 2027, OLED is expected to account for 31% of them. Meanwhile, high-end LCD TV shipments actually rose last year, by 4%, and will grow at a CAGR of 8% through 2027, reaching 20.7 million units.

All told, premium TV sales are expected to grow at a CAGR of 7% between now and 2027, with revenues set to top $23.9 billion by the end of that year. OLED TV sales will account for $10.9 billion of those sales, while high-end LCD TV sales will reach $16.7 billion.

MicroLED TVs only accounted for a 0.1% share of the premium TV market based on shipment volume in 2023. Nonetheless, the technology is expected to catch on fairly rapidly in the coming years, with DSCC saying it will account for $1.7 billion in sales by 2027 and a 6% share of the market.

In a comparison between OLED TVs and Mini-LED TVs, OLED leads the way in both shipments and sales, DSCC said. While Mini-LED TV sales have grown rapidly since 2021, thanks to their price competitiveness, OLED will continue to dominate the segment until 2027, when Mini-LED will finally surpass the technology and take a 50.4% market share.

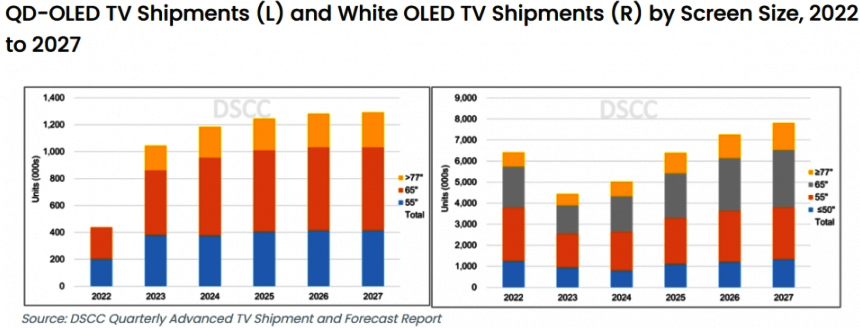

Within the OLED TV market, there are two kinds of display technology, with LG Display’s WOLED and Samsung Display’s QD-OLED panels vying for dominance. QD-OLED is the more expensive of the two technologies, but WOLED panels are used by many more brands and therefore found in far more products.

According to DSCC, QD-OLED had a 19% market share in 2023 in terms of shipments, and this is expected to increase slightly to 20% this year. However, its share will then decline gradually each year through 2027, as a result of Samsung Display’s limited production capacity. By 2027, QD-OLED will account for just 14% of total sales within the OLED category.

On a regional basis, North America and Western Union will account for the bulk of sales in the premium TV market through 2027, although their dominance will gradually decrease over the duration of the forecast period. Meanwhile, Asia’s market share will gradually increase, DSCC said.